How disruption in the Strait of Hormuz threatens fertilizer supply and global food prices

Shipping through the Strait of Hormuz sharply declined in early March after escalating conflict in the Gulf disrupted commercial navigation through the narrow corridor between Iran and Oman. While the strait is widely known as one of the world’s most important oil routes, it also connects natural gas exports from Gulf producers to global fertilizer production and agricultural supply chains. Disruptions affecting this corridor can therefore propagate beyond energy markets and influence fertilizer availability, agricultural input costs, and ultimately food prices worldwide.

Satellite image showing Strait of Hormuz on February 21, 2026. Credit: CopernicusEU/Sentinel-2, The Watchers

- The Strait of Hormuz is widely known as a major oil transit route, but it also sits at the center of a supply chain linking natural gas exports to fertilizer production and global agriculture.

- Natural gas is used to produce ammonia through the Haber–Bosch process, the chemical basis of most nitrogen fertilizers used in modern farming.

- Because fertilizer feedstocks and finished fertilizers move through the same corridor, disruptions affecting shipping in the Strait of Hormuz can influence fertilizer supply, agricultural costs, and ultimately food prices.

Navigation through the Strait of Hormuz has sharply declined as conflict in the Gulf disrupts commercial shipping through the narrow corridor between Iran and Oman that connects the Persian Gulf with the Gulf of Oman and the Arabian Sea.

The current disruption follows U.S. and Israeli military strikes on Iran that began in late February 2026, including attacks on Iranian nuclear and military infrastructure. Iranian forces subsequently targeted energy facilities inside Qatar, striking QatarEnergy’s operational sites at Ras Laffan Industrial City and Mesaieed Industrial City.

At the same time, Iran’s Islamic Revolutionary Guard Corps issued radio warnings prohibiting commercial vessel passage through the strait, and tanker traffic fell by approximately 70% within days before reaching near-zero levels.

Major shipping operators, including MSC, CMA CGM, and Hapag-Lloyd, formally suspended all Hormuz transits, and roughly 170 containerships carrying an estimated 450 000 TEU of cargo were reported stranded in the region as of early March 2026. Brent crude rose by up to 13% in response to the halt in traffic.

The Strait of Hormuz and its role in global fertilizer supply

The strait functions as the main export route for energy shipments from Gulf states, including crude oil, liquefied natural gas (LNG), and petrochemical products.

Because the exports include natural gas and chemical feedstocks used in fertilizer manufacturing, disruptions at this chokepoint can propagate through energy, industrial chemical, and agricultural supply chains.

According to Kpler commodity tracking data, approximately one-third of globally traded fertilizer, including nitrogen, phosphate, and sulphur, transits the Strait of Hormuz each month, representing 3 to 3.9 million tonnes of fertilizer exports.

Analysts at the Fertilizer Institute estimate that roughly half of global seaborne sulphur exports originate from the Middle East Gulf and must pass through the strait. Sulphur is a primary raw material for producing sulphuric acid, which is required for phosphate fertilizer manufacturing, meaning a Hormuz closure affects not just nitrogen supply but the entire phosphate fertilizer chain simultaneously.

Morocco, a major global exporter of phosphate fertilizers, depends on Gulf sulphur and ammonia imports to sustain its production, creating second-order disruption to phosphate markets well outside the immediate conflict zone.

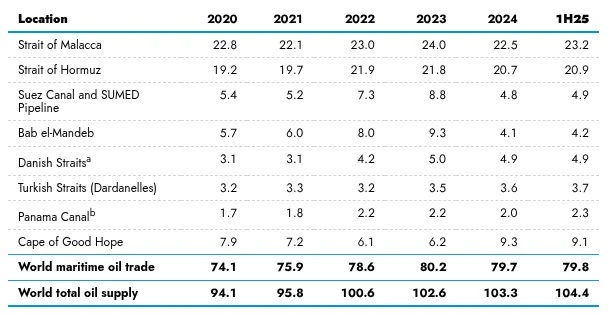

The Strait of Hormuz carries one of the largest concentrations of energy trade in the global maritime system, with energy analysts estimating that roughly one-fifth of global petroleum liquids consumption and a significant share of international liquefied natural gas exports transit the corridor each day.

The strait is deep enough and wide enough to handle the world’s largest crude oil tankers, and it is one of the world’s most important oil chokepoints, according to the U.S. Energy Information Administration. “Large volumes of oil flow through the strait, and, if it were to be closed, alternatives that exist could move only a portion of the oil volumes out of the strait.”

Data source: U.S. Energy Information Administration (EIA), Short-Term Energy Outlook, February 2026, and EIA analysis based on Vortexa tanker tracking and Panama Canal Authority data, using EIA conversion factors and calculations

Note: World maritime oil trade excludes intra-country volumes except those volumes that transit global chokepoints and the Cape of Good Hope. 1H25=first half of 2025

a) The Danish Straits do not include flows through the Kiel Canal.

b) Data for the Panama Canal are by fiscal year (October 1 to September 30)

Gulf states, including Qatar, Saudi Arabia, the United Arab Emirates, and Oman, depend on this route for energy exports that supply markets across Asia, Europe, and Africa. Because natural gas exported from this region is also used as feedstock for ammonia production, disruptions affecting traffic through the strait can influence both global energy markets and nitrogen fertilizer supply chains.

On March 3, QatarEnergy, the world’s largest LNG producer, confirmed it had halted production of LNG and all associated downstream products at its Ras Laffan and Mesaieed industrial facilities following direct military strikes. The suspension explicitly covers urea, methanol, polymers, and aluminium, removing a significant volume of urea from global markets at the start of the Northern Hemisphere spring planting season.

Qatar is among the world’s largest urea exporters, and its output supplies import-dependent agricultural economies across Asia and Latin America. Urea prices in the United States, Brazil, and the Middle East increased immediately following the escalation, with Saudi producers raising benchmark urea prices from approximately $402 to $450 per tonne FOB.

Natural gas and the fertilizer production chain

Modern agriculture relies heavily on nitrogen fertilizers produced from ammonia synthesized through the Haber–Bosch process. Because this process consumes large quantities of natural gas, fertilizer production costs and output remain closely tied to natural gas availability and price.

Disruptions affecting navigation through the strait could therefore influence both energy supply and fertilizer trade simultaneously, and timing plays an important role in determining the agricultural consequences of fertilizer supply disruptions.

In the Northern Hemisphere, fertilizer application for many staple crops typically occurs between March and May, followed by planting during April through June. Farmers rely on fertilizer availability during this period to support early crop development and nutrient uptake.

If fertilizer shipments are delayed during this application window, farmers may adjust fertilizer application rates or rely on available inventories. Reduced nitrogen application can influence crop growth later in the season because nitrogen availability affects vegetative development, grain formation, and overall yield potential.

What the disruption could mean for consumers and food markets

For most consumers, the immediate impact of disruptions affecting fertilizer supply chains is not food shortages but higher food prices. Fertilizer is one of the largest input costs in modern agriculture, particularly for crops such as wheat, maize, rice, and oilseeds.

When fertilizer prices rise because of higher natural gas costs or supply disruptions, those higher costs are passed through the agricultural supply chain.

Farmers in major producing regions often continue using fertilizer even when prices increase, because reducing nutrient application can lower crop yields. As a result, higher fertilizer costs tend to translate into higher production costs for grains and other staple crops. The costs later appear in food markets as increased prices for products ranging from bread and cereals to meat and dairy, which rely on grain-based animal feed.

Countries with large domestic natural gas supplies and fertilizer production capacity, such as the United States, are generally less vulnerable to supply shortages, although farmers may still face higher fertilizer prices if global energy markets tighten. European agriculture can also experience cost increases because fertilizer production there depends heavily on natural gas prices in regional energy markets.

Brazil, the world’s largest soybean exporter and a major corn producer, imports approximately 8 million tonnes of urea annually, a significant share of which originates from Gulf producers. Saudi Arabia’s Ras Al-Khair port was loading an estimated 80 000 to 85 000 tonnes of DAP and MAP phosphate fertilizers bound for Latin America in the period when commercial transit through the strait collapsed, and those shipments must transit the Hormuz corridor to reach their destination.

A disruption affecting Brazilian soybean and corn input costs carries downstream consequences for global oilseed and feed grain markets beyond what South Asian or African import exposure alone would generate.

Even greater exposure is often found in countries that rely heavily on imported fertilizers, like large agricultural economies in South Asia, including India and Pakistan. Many countries in sub-Saharan Africa and parts of Southeast Asia also depend on imported fertilizer supplies and have less financial capacity to absorb sudden price increases.

In those regions, sharp fertilizer price spikes can sometimes lead farmers to reduce application rates, which may affect yields during the growing season.

Because fertilizer is applied early in the agricultural cycle, disruptions during the main Northern Hemisphere fertilization period between March and May can be particularly sensitive. If supply constraints coincide with this window, fertilizer prices and availability can influence planting decisions and input use for the season’s crops.

Structural difference between energy and fertilizer supply disruptions

A key structural difference between energy and fertilizer supply disruptions is the absence of any strategic reserve mechanism for fertilizers. Unlike crude oil, for which governments maintain strategic petroleum reserves measured in months of consumption, there is no equivalent buffer for urea, ammonia, or phosphate fertilizers.

When supply is disrupted during the Northern Hemisphere spring application window, farmers cannot draw on government stockpiles and must rely entirely on commercially held inventory, which in many import-dependent countries is held at port-level stocks measured in weeks rather than months.

The simultaneous closure of the Strait of Hormuz and resumption of Houthi attacks on Red Sea shipping, eliminating both primary routing options for Gulf energy exports, removes the rerouting flexibility that allowed partial adaptation during previous single-corridor disruptions.

Houthi attacks had paused around November 11, 2025, following a Gaza ceasefire deal, giving roughly 3.5 months of relative Red Sea calm. On February 27, 2026, two senior Houthi officials announced they would restart missile and drone operations in direct response to the U.S.-Israeli strikes on Iran.

While the global food system has historically adjusted to supply disruptions through trade and production shifts, the interconnected nature of energy, fertilizer, and agriculture means that disturbances in key infrastructure corridors such as the Strait of Hormuz can propagate beyond energy markets and eventually affect agricultural costs and food prices worldwide.

References:

1 World Oil Transit Chokepoints – EIA – Accessed March 4, 2026

2 Nitrogen (Haber–Bosch and fertilizer chemistry) – Royal Society of Chemistry – Accessed March 4, 2026

3 Global fertiliser dependency on Gulf exports: what if Hormuz is disrupted? – Kpler – June 18, 2025

4 Erisman, J., Sutton, M., Galloway, J. et al. How a century of ammonia synthesis changed the world. Nature Geosci 1, 636–639 (2008). https://doi.org/10.1038/ngeo325

5 QatarEnergy Ceases LNG Production Following Military Offensive – Qatar News Agency – March 2, 2026

6 RPT About 10% of the global container ships caught in Gulf of Hormuz backup, ONE CEO says – Reuters – March 2, 2026

7 Strait of Hormuz transits collapse as shipping’s risk appetite is tested – Lloyd’s List – March 2, 2026

I'm a dedicated researcher, journalist, and editor at The Watchers. With over 20 years of experience in the media industry, I specialize in hard science news, focusing on extreme weather, seismic and volcanic activity, space weather, and astronomy, including near-Earth objects and planetary defense strategies. You can reach me at teo /at/ watchers.news.

Commenting rules and guidelines

We value the thoughts and opinions of our readers and welcome healthy discussions on our website. In order to maintain a respectful and positive community, we ask that all commenters follow these rules.